Do you know anyone with an arm or two?

Wait, an ARM, as in an Adjustable Rate Mortgage? Probably a smaller group now…

Despite the bad rap ARMs got during the housing meltdown, they’re not all bad. In fact, only a relatively small percentage of them were usurious. If you had a standard ARM and you’ve been riding it from 2009 to now, you’ve probably done pretty well. I have one, and I don’t plan on refinancing out of it. But? My metrics and parameters may be wildly different than anyone else’s.

There are a variety of factors to consider when evaluating whether to take an Adjustable Rate Mortgage vs. a fixed loan. Likewise, if you have an ARM it’s not one size fits all as to when, or if, you’ll want to refinance out of it.

Until the housing market crash, that pushed mortgage rates to historic lows, it was generally true that ARMs out-performed 30yr fixed mortgages, if you had the stomach and ability to ride the ups and downs (and refinance if needed). Is that true now? I doubt it. If you’ve secured long-term financing between 3% and 4.5% that we’ve enjoyed for the last year or two, I can’t imagine ARMs outperforming that, over the long haul.

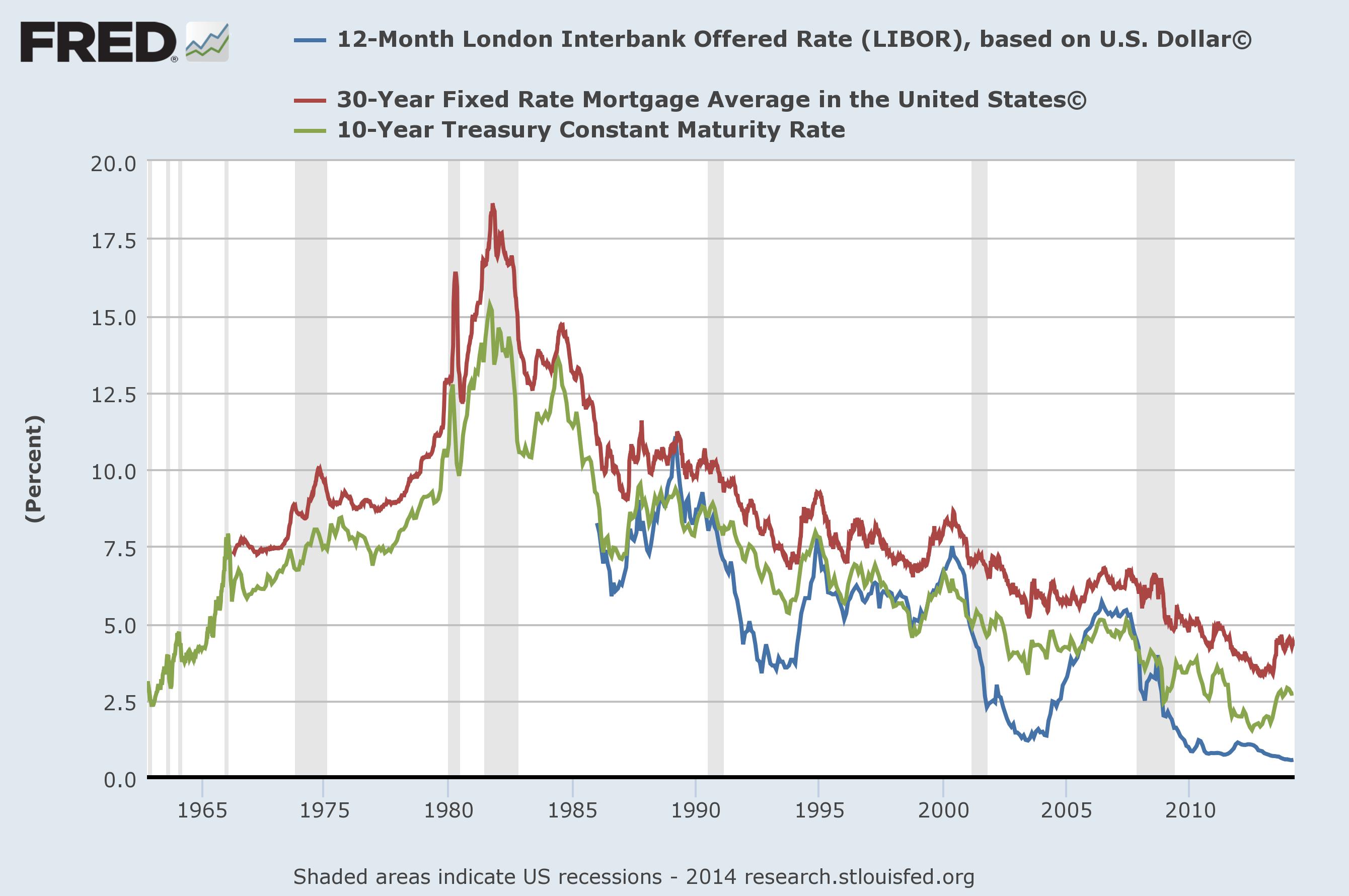

Have a look at this chart:

It’s a snapshot of 30yr fixed mortgage rates and two common indices upon which ARMs are based, the 12-month LIBOR and the CMT (constant maturity treasury). There are several other indices that an ARM may be based upon, but it really doesn’t matter. Every index will follow a very similar pattern as those seen here. Find out what yours is, and look it up.

Granted, past performance is not an indication of future results, but? To me, it looks pretty clear that rates are unlikely to go lower, and most likely they will continue climbing from current lows. How fast, and how far? That’s anyone’s guess.

Be sure to also know the margin of your ARM, which is what the bank charges on top of your index. In my case, the index is the 12-month LIBOR, with a 2.25% margin. My ARM can only adjust up or down by 2%/yr, regardless of what the underlying index does.

So, if you’ve got an ARM now, what should you do?

It depends.

When did you take out that ARM? When is your first, or next adjustment? How long do you plan on keeping that property? How big is your principal balance? How comfortable are you, or how uncomfortable would you be, IF rates rise and drive your payment up? Do you have an option to refinance, if that were to happen? What sort of caps do you have – if any – on your ARM (there are typically caps for your first adjustment, annually, and life of loan)?

My ARM has worked out pretty well, so far…

Did I see rates going as low as they did when I bought a property w/ a 3/1 ARM in 2006? Not a chance. But, even though I bought the place with a buy and hold mentality, I was taking a calculated risk that my ARM would outperform a 30yr fixed rate, which was in the 6%s at that time.

Good luck definitely helped, because although the duplex I bought lost 50% of its value, during the crash, precluding me from any viable refinance options – until HARP II was rolled out, pretty late in the game – since my rate and payment went so low, by continuing to pay the same as I’d started with, I hacked my principal balance way faster than any fixed loan would’ve allowed for similar payments. That was a nice bonus.

I’ve paid down about $33k of principal since I bought the place in 2006. Had I used 30yr fixed financing, with rates in the 6%s at that time, I’d have spent the same cash, and have a balance of roughly $118k vs. my $99k outstanding now. And, due to the lost equity, I wouldn’t have been able to keep refinancing as fixed rates plunged.

Fortunately, at this point, with only $99k outstanding, even if rates rise faster than I think they may, my payment will still be manageable, since my rents cover, or theoretically cover – those of you with rental properties may be able to relate there – my payment.

Lastly, I’m “guessing” that the LIBOR will remain relatively low for another two years. I’ve done the math. If I were to refinance with a HARP II 15yr fixed (unfortunately, I can’t do Georgia loans – well, I guess I could get licensed there, but that’s another story) I’d be at about 4.5% because the rate/fees I can find through other lenders aren’t as good as what I could get myself. My payment would pretty closely match what I’m paying now, but? If I’m right, and the LIBOR doesn’t climb too much in the next two years, I’ll actually cut an extra $5k or so off my principal in the next two years riding my ARM vs. taking a 15yr fixed loan today.

At that point, I’ll owe about $80k, so even if the place is worth about the same as today (maybe $100k) I’ll have refinance options at that time – if I need them. At 3.25% (and I’m actually at 2.875%) with 22 years remaining my required principal and interest payment is $525/mo. Even if rates rise precipitously, so I’m paying 7% with 20yrs remaining on $95k, my payment would still be a very manageable $736/mo. On the other hand, if we find rates are still riding their lows two years down the road? I’ll do the math again, and may continue riding that ARM.

But, if I had $300k or more on the line? You bet I’d be doing the math very seriously about whether to refinance or not with fixed rates near their historic floor. $300k at 3.25% with 22 years remaining is $1592/mo, and $280k at 7% with 20 years remaining jumps to $2170. That’s a sizeable monthly increase. Is it worth taking that chance of rates staying low?

Unfortunately, we’ll know in five or ten years what the right call was. Isn’t hindsight great?!

So, if you’re riding out an ARM – or you know anyone that is – and want some insight into whether or not a refinance would pencil out well, while fixed rates are still really close to their historic floor, give me a call.

Likewise, if you’re considering using an ARM vs. a fixed loan now, and want a candid and objective analysis of whether an ARM or a fixed mortgage would serve you best, don’t hesitate to call.

In the meantime, here are your rates for this week. Please don’t hesitate to call or email if you, your friends, or family have questions about financing residential or commercial real estate.

Cheers!

E

| Conforming | Rates | Points | APR | Loan Amt | Payment | |

| 30 yr fixed mortgage | 4.250% | 0 | 4.250% | $ 300,000.00 | $ 1,476 | |

| 15 yr fixed mortgage | 3.250% | 0 | 3.250% | $ 300,000.00 | $ 2,108 | |

| 3/1 ARM | 3.500% | 0 | 3.500% | $ 300,000.00 | $ 1,347 | |

| 5/1 ARM | 2.875% | 0 | 2.875% | $ 300,000.00 | $ 1,245 | |

| Jumbo (ask me about Super Conforming limit, per your zip code) | ||||||

| 30 yr fixed mortgage | 4.625% | 0 | 4.625% | $ 550,000.00 | $ 2,828 | |

| 15 yr fixed mortgage | 4.000% | 0 | 4.000% | $ 550,000.00 | $ 4,068 | |

| 3/1 ARM | 3.750% | 0 | 3.750% | $ 550,000.00 | $ 2,547 | |

| 5/1 ARM | 3.750% | 0 | 3.750% | $ 550,000.00 | $ 2,547 | |

| Rates subject to change without notice. | ||||||

| Please keep in mind, these rates and statistics are for informational purposes only to give you a sense of market movement and my opinion as to why. Although these rates exist today, based on certain qualifying characteristics (740+ fico, owner occupied SFR with 75% loan to value ratio or less), your scenario may allow for lower or higher interest rates. Licensed by the CA Dept of Real Estate, #01760965. NMLS: 239756. Equal Opportunity Housing Lender. If you’d like to be removed from this list, please reply with REMOVE in the subject line. You can also use this link, mailto:eric@ezmortgages.us and add REMOVE to the subject line. To add someone who would appreciate this information, send me their email with SUBSCRIBE as subject. | ||||||

Eric Grathwol

Broker

EZ Mortgages, Inc.

4535 Missouri Flat Rd. Ste. 2E

Placerville, CA 95667

Office: 530-303-3643

Cell: 916-223-4235

Fax: 530-237-5800

NMLS: 239756

www.ezmortgages.us