Happy New Year!

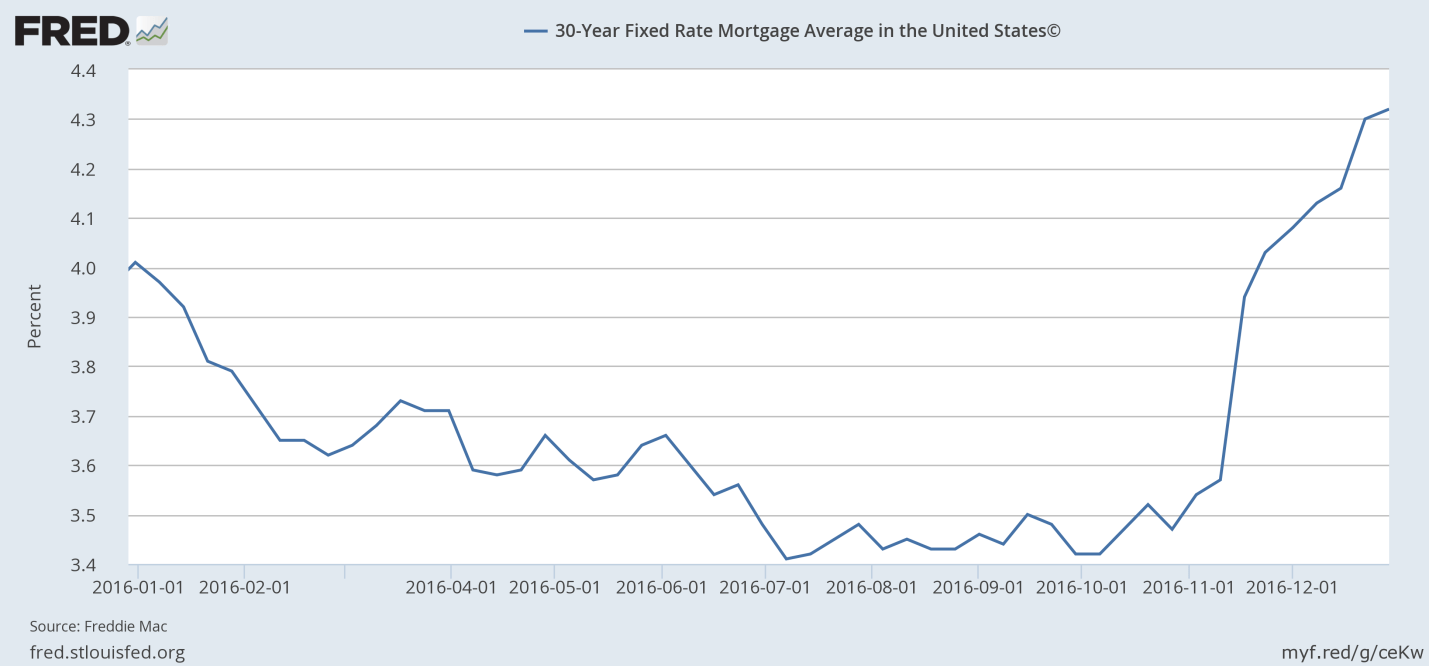

Wow. Another one in the books. Is it just me, or do the years seem to pass by faster each time? As to mortgage rates, take a look at this snapshot of recent activity:

That’s what the average 30yr fixed mortgage rate has done, in the wake of the Presidential Election and Trump becoming our President Elect. It’s even more interesting, because the eve of the election, most analysts and pundits were predicting the exact opposite, IF Trump were to win. So much for analysts and punditry.

So, is this finally the point where the economy picks up, interest rates rise, and never look back?

Honestly, I have no idea. Although I may be in the minority, this time, I’m increasingly of the mind that won’t be the case. Yet.

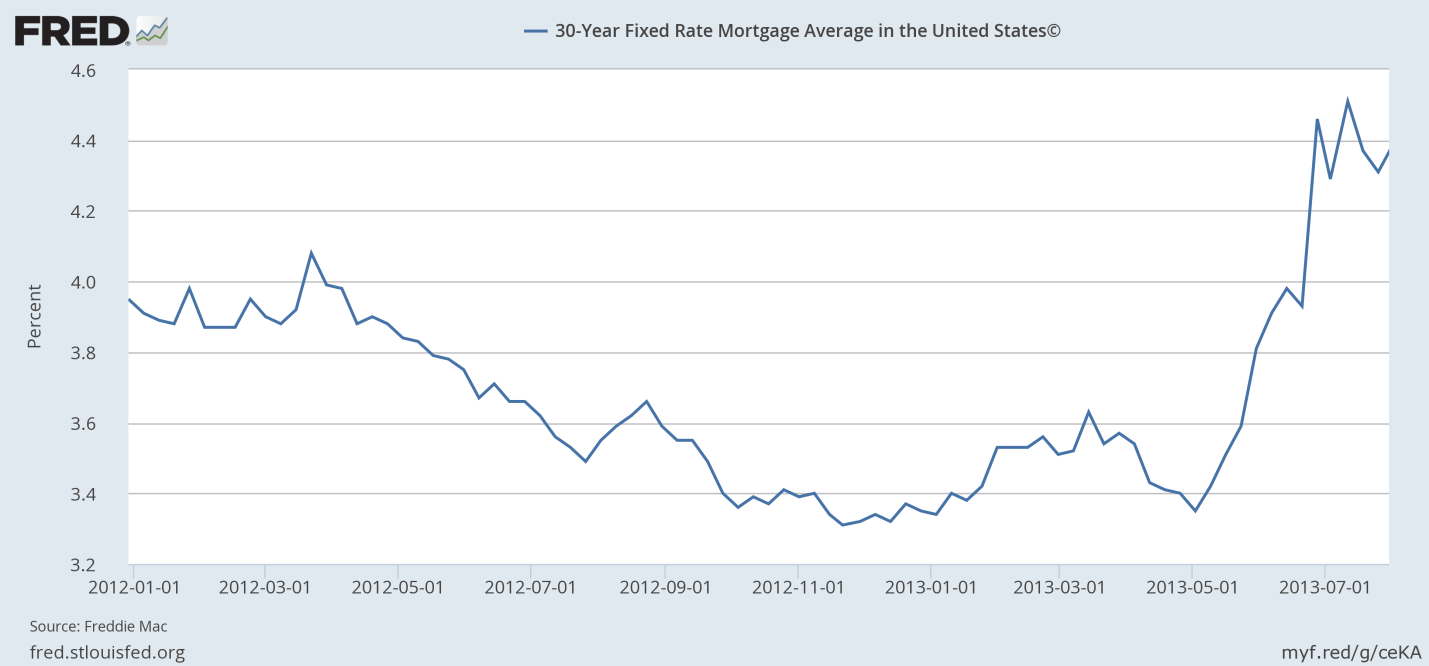

For some perspective, let’s look at May 2013, now referred to as the Taper Tantrum, when then Federal Reserve Chairman Ben Bernanke told us, and I’ll paraphrase “at some point, economic conditions will warrant a shift to more normal monetary policy”:

It’s a very similar spike to the one we’re in now. At that time, I thought we were lifting off the floor for good. As history has proven, I was wrong. There still wasn’t enough economic growth to achieve escape speed.

Since then, rates basically did nothing but drift lower, with the exception of a few isolated, and eventually temporary, spikes.

As you’ll commonly hear when looking at economic and financial metrics, past performance may not be indicative of future results.

So, what will the future hold? It’s anyone’s guess.

One economist I like to read, David Rosenberg of Gluskin Scheff, recently put it this way, again I’m paraphrasing “nothing has changed, other than we have a President Elect who may be somewhat volatile and unpredictable.”

Although Trump, like nearly every President Elect, has pivoted from many of his talking points during the election, by looking at his choice of Cabinet posts and advisors, we’re getting a sense of what tone for policy they are likely to try to set: Lower taxes, less regulation, while increasing defense and infrastructure spending (the latter was largely in place but largely blocked by Congress the last 8 years).

Although the goal of those policies is to spur growth, increase Federal revenue, and cut the deficit, it’s unclear whether that can all come to fruition. There’s fear that the budget deficit may grow, not shrink. The ripple effects on growth through the economy may or may not materialize, and this, in turn, could stoke inflationary pressure, without much economic growth (except for the few who directly benefit from that increased spending).

It’s also true that in most cases, the President of the United States has much less direct impact on the economy than most people think. They tend to inherit, and get the bulk of the credit or blame for, the economic cycle driven by the preceding years. They can set the tone, but there are too many variables beyond their control, and events that they have to react to, that do as much, if not more, to drive the end result than their policy goals coming into office.

An economic system as large as the United States’ doesn’t turn on a dime. It can take several months, or even years for the impact of fiscal policy to ripple through to bottom line impact. Many people believe our next recession may not be far away, regardless of what policies the Trump Administration can implement.

I think we’ll learn a lot over the next month or three, after Donald J Trump actually takes office, about what policies may or may not take shape, and begin to get a sense of their impact on the economic gears of the United States. As every administration finds, we’ll no doubt have some unforeseen events, to which they have to react, that may or may not drive policy in the same direction they’d originally planned.

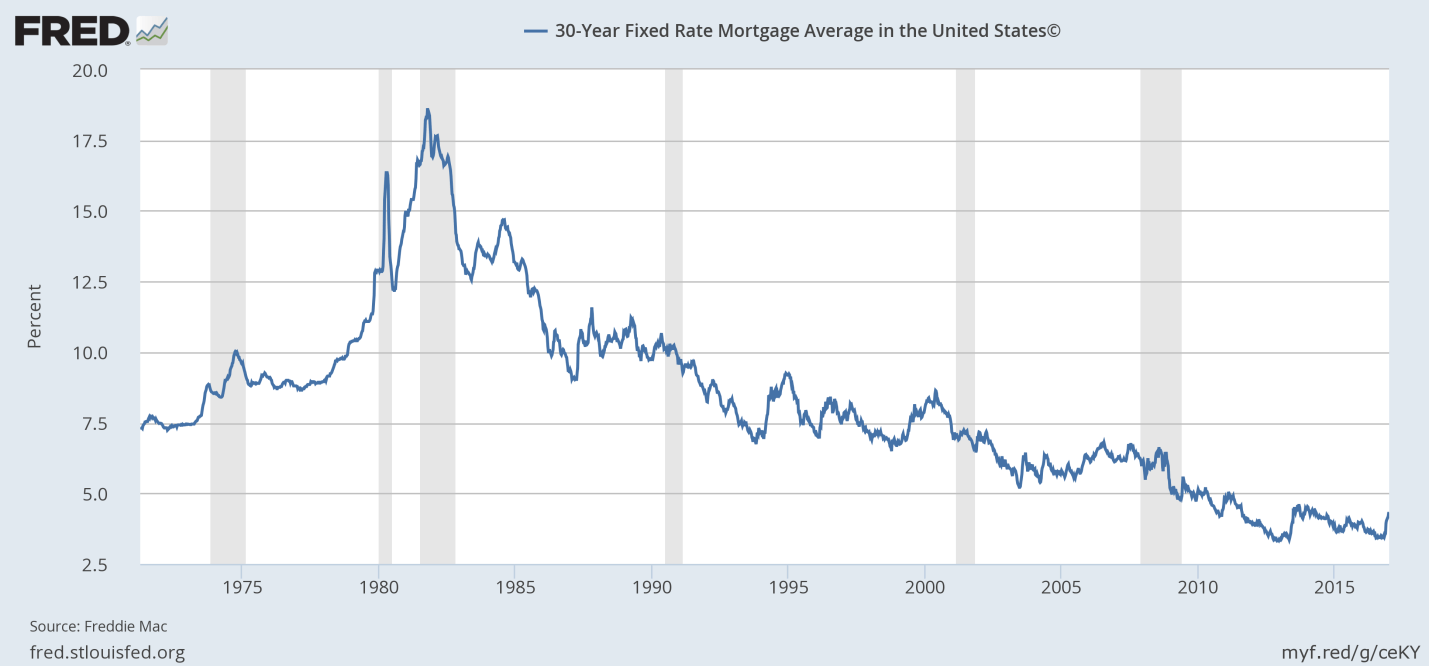

As all that relates to mortgage rates, stepping back, taking the long view, we can see that we’ve been in the midst of an almost forty year decline. At some point, that decline will end.

We know, with certainty, rates will not stay low forever. But, nobody has any idea when the underlying economic fundamentals will drive them to move higher, and never look back. Ten years ago, nobody would believe you could get 30yr fixed mortgages, at 3.5%-4%, with no points, and no fees. Let alone that rates would be that low for years. Yet, for a generation of buyers, and homeowners, that’s practically all they know.

Although the current spike seems massive in the moment, and it’s a good sized one, when we step back, it “could” just be another blip as the world and US Economies continue to find their way, evolving into, and taking shape from the realities of the new millennium that may be driven more by demographics and globalization than any governmental policy. They key for this administration, and the next several, may be recognizing those realities, and doing what can be done to shape policy to benefit the most people within those larger forces.

I’ll do my best to keep you posted as we roll into the New Year, and beyond. Please don’t hesitate to call or email if you, your friends, clients, or family have questions about buying or refinancing residential or commercial real estate.

Best wishes to you and yours for a happy, healthy and prosperous 2017.

Here’s how our rates ended this week (they actually drifted slightly lower this week, than they started; we’ll see what the New Year brings).

Cheers!

E

| Conforming | Rates | Points | APR | Loan Amt | Payment |

| 30 yr fixed mortgage | 3.990% | 0 | 4.040% | $ 300,000.00 | $ 1,431 |

| 15 yr fixed mortgage | 3.250% | 0 | 3.350% | $ 300,000.00 | $ 2,108 |

| 3/1 ARM | 4.500% | 0.5 | 4.750% | $ 300,000.00 | $ 1,520 |

| 5/1 ARM | 3.375% | 0 | 3.425% | $ 300,000.00 | $ 1,326 |

| Jumbo (ask me about Super Conforming limit, per your zip code) | |||||

| 30 yr fixed mortgage | 4.500% | 0 | 4.530% | $ 550,000.00 | $ 2,787 |

| 15 yr fixed mortgage | 4.000% | 0 | 4.030% | $ 550,000.00 | $ 4,068 |

| 3/1 ARM | 4.625% | 0 | 4.655% | $ 550,000.00 | $ 2,828 |

| 5/1 ARM | 3.750% | 0 | 3.780% | $ 550,000.00 | $ 2,547 |

| Rates subject to change without notice. | |||||

| Please keep in mind, these rates and statistics are for informational purposes only to give you a sense of market movement and my opinion as to why. Although these rates exist today, based on certain qualifying characteristics (760+ fico, owner occupied SFR with 75% loan to value ratio or less and $250,000+ loan amount), your scenario may allow for lower or higher interest rates. Licensed by the CA Dept of Real Estate, #01760965. NMLS: 239756. Equal Opportunity Housing Lender. If you’d like to be removed from this list, please reply with REMOVE in the subject line. You can also use this link, mailto:eric@ezmortgages.us and add REMOVE to the subject line. To add someone who would appreciate this information, send me their email with SUBSCRIBE as subject. | |||||

Eric Grathwol

Broker

EZ Mortgages, Inc.

4535 Missouri Flat Rd. Ste. 2E

Placerville, CA 95667

Office: 530-303-3643

Cell: 916-223-4235

Fax: 530-237-5800

NMLS: 239756

www.ezmortgages.us